Insights

Portfolio Insights

Portfolio Spotlight: Amutus

Market Views

Private Credit Explained: Market Risks, Returns & What the Headlines Miss

Market Views

What’s Really Happening In Private Credit?

Market Views

Private Credit: Myth vs. Fact

Firm News

Introducing Tommy Fleetwood, our first Global Brand Ambassador

Market Views

Jon Gray on His Confidence in Private Credit’s Enduring Premium

Market Views

Jon Gray at Top Advisor Conference Breaks Down Facts on Private Credit

Market Views

Decoding the Real Estate Cycle

Portfolio Insights

Propelling the Growth of Leading Franchisors

Market Views

Market Views: Dealmaking, Disruption, and Real Estate’s Recovery

Market Views

Why Should You Care About Data Centers?

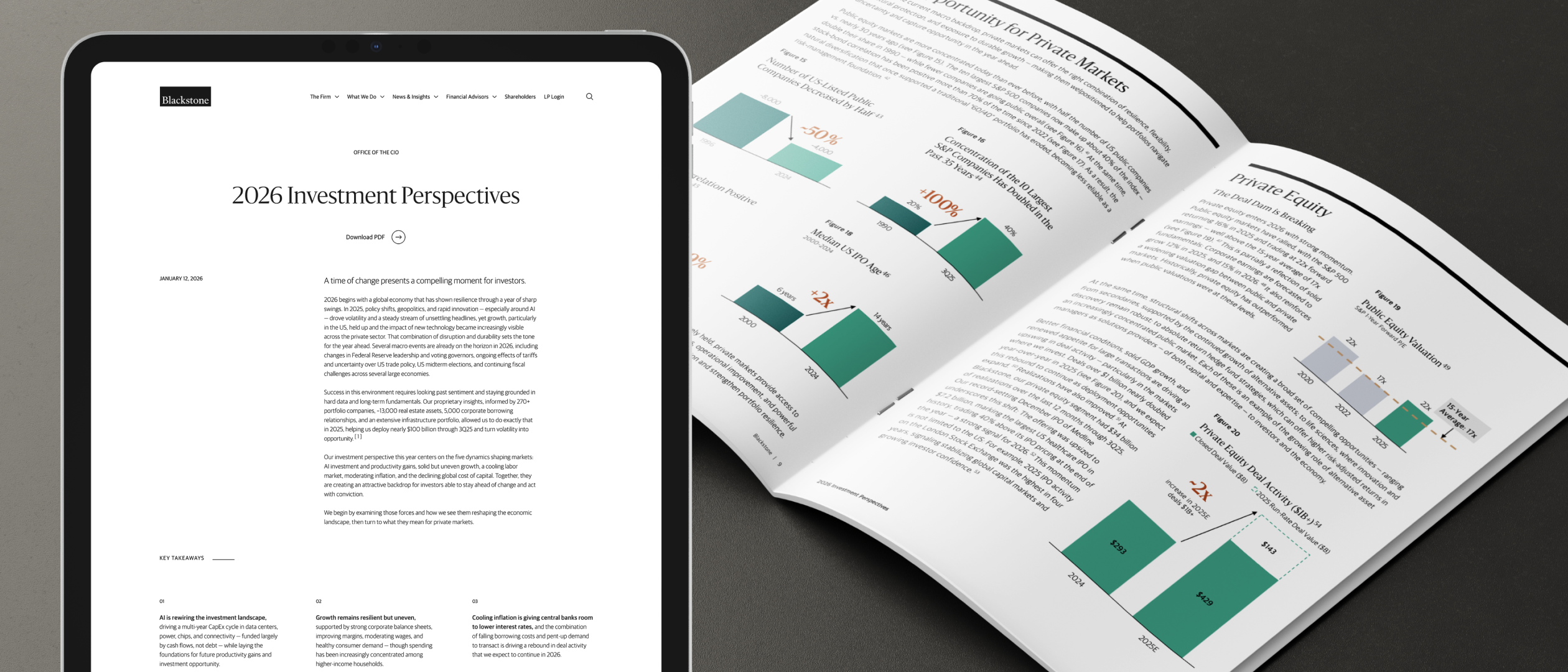

Investment Strategy

2026 Investment Perspectives

Insight