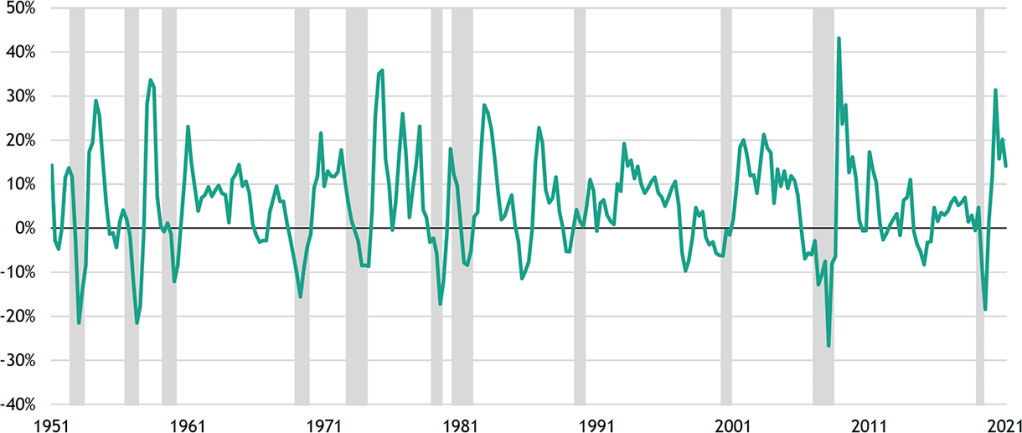

Sufficient conditions for a recession lacking The first condition is an earnings recession. As Figure 1 shows, corporate profit growth turns negative before a recession. The modern US economy has never had a recession when profit growth is positive. Growth slowdowns in Europe and China, from which many large multinational companies derive most of their revenues, are concerning. However, the profits outlook is still relatively strong, despite slowing growth and tougher comps. Blackstone portfolio company CEOs are generally optimistic about revenue EBITDA growth, with the vast majority expecting continued year-over-year growth in both categories this year and in 2023.[2]

Figure 1: US Corporate Profit Growth (YoY change)

Source: Blackstone Investment Strategy and Bureau of Economic Analysis, as of December 31, 2021. Represents corporate profits before tax with inventory valuation and capital consumption adjustments.

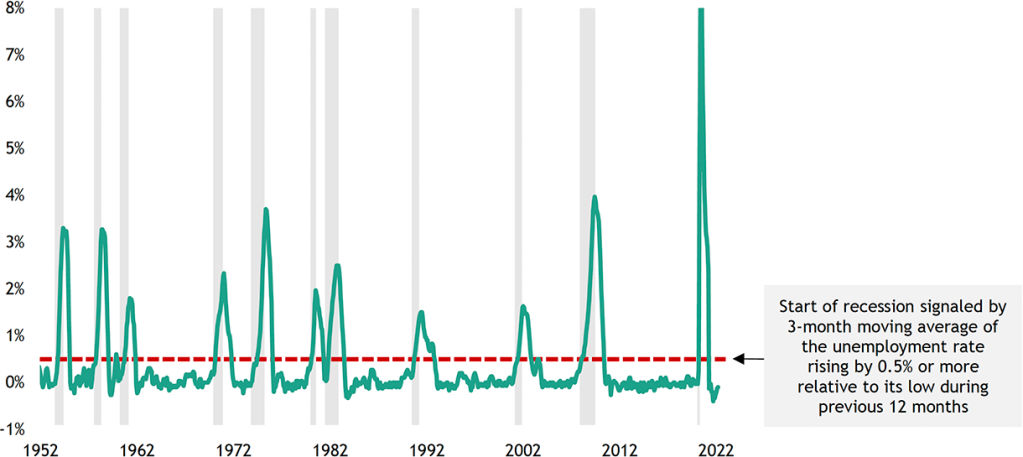

The second precondition is a back-up in the unemployment rate. Figure 2 highlights the Sahm Rule Recession Indicator, named for former Fed researcher Claudia Sahm. This indicator suggests that we remain quite far from labor market conditions that would signal the start of a recession. The number of people filing for first-time unemployment is at historic lows, levels not seen since the 1960s. Meanwhile, the number of job openings remains at historic highs in absolute terms, with roughly 1.7 unfilled jobs for every unemployed person.

Figure 2: Sahm Rule Recession Indicator (3-month moving average of the unemployment rate, relative to its low during previous 12 months)

Source: Blackstone Investment Strategy, Bureau of Labor Statistics and Claudia Sahm, as of March 31, 2022.

Reasons to be optimistic about growth As I’ve mentioned, I do find the recent yield curve inversion is troublesome, but the economy still has momentum. Household balance sheets remain strong, labor markets are robust, and companies are reluctant to let go of employees. Also, profit growth remains on track to increase. As a result, I will take the “over” on economic growth and the “under” on recession risk, as I think this cycle has a longer runway still.

Investment Strategy

The 40% Problem

June 24, 2025