At a Glance

Government incentives to foster economic growth are nothing new. From the development of the oil and gas sector in the early 20th century to the implementation of research and development programs through the tax code beginning in the 1980s, we have seen numerous examples. Today, the government aims to modernize supply chains and sophisticated manufacturing through the Inflation Reduction Act (IRA), CHIPS and Science Act, and Infrastructure Investment and Jobs Act (IIJA).

Broadly speaking, I expect these historic bills, in combination with nearshoring and onshoring macro trends, to be positive for commodities, infrastructure, transportation, housing and logistics. However, the undercurrents of inflation and undersupplied labor markets can’t be discounted when assessing the potential economic impact.

Supply chains were already in flux Companies began contemplating supply chain diversification in 2018 when the trade wars with China escalated. Some companies redirected their operations to Vietnam and Indonesia, but few completely severed ties with China. Attitudes shifted with COVID. A survey of global supply-chain leaders conducted by McKinsey found that 42% of CEOs adjusted their company’s supply chains, up from just 15% in 2020. [ 1 ] Global trade flows in 2023 support this trend: Through June, Mexico and Canada surpassed China to become the primary and secondary suppliers of goods to the US. Foreign Direct Investment (FDI) flowing into Mexico surged at an annual rate of 41% to reach USD 29 billion during the first half of 2023, double the average of the past 15 years[ 2 ] Similarly, in Canada, FDI witnessed a substantial increase of 19% year-on-year, matching Mexico’s total of USD 29 billion in the first half of 2023.[ 3 ]

Investment = growth Since the passage of the IRA and the CHIPS Act in August 2022 and the IIJA in November 2021, there have been approximately 37,000 announcements of new manufacturing, infrastructure, and clean energy projects, representing over $800 billion in new investments.[ 4 ] The dividends of these investments will resonate throughout the economy for years to come. Nonresidential construction has one of the highest multiplier effects of any industry in the United States; for every $1 in direct spending, there is over 3x that in related spending.[ 5 ]

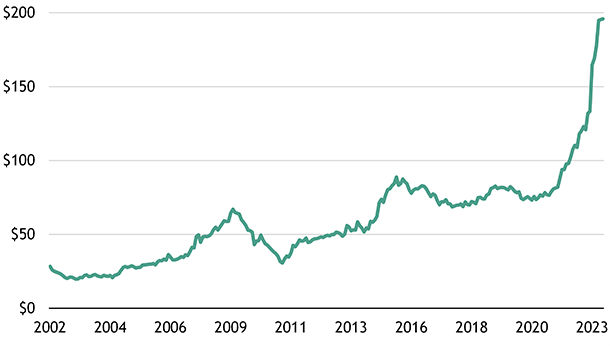

Figure 1: Total US Manufacturing Construction Spending

($ in billions; seasonally adjusted annualized rate)

Source: US Census Bureau, as of 7/31/2023

Source: US Census Bureau, as of 7/31/2023The distribution of these projects warrants attention, as the effects won’t be experienced uniformly. US economic activity had already begun shifting towards the southern and southwestern regions, and the emergence of new projects seems to build on that momentum (see Figure 2). The changing economic map will likely not only influence other shifts within the United States, but also continue to reconfigure global supply chains towards Mexico and Canada.

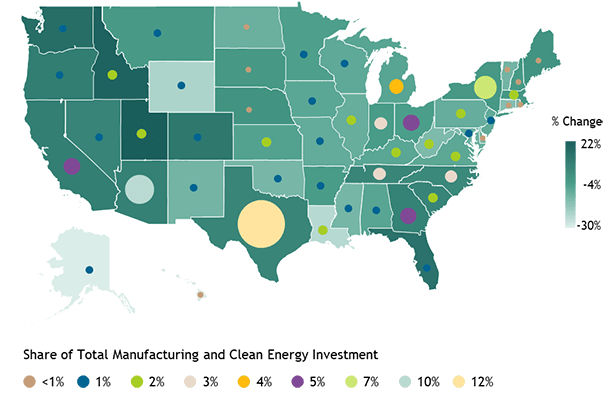

Figure 2: Change in State Share of National GDP

(2012-2022)

Source: US Bureau of Economic Analysis (7/31/2022), The White House (8/15/2023) and Macrobond.

Source: US Bureau of Economic Analysis (7/31/2022), The White House (8/15/2023) and Macrobond.Commodities readying to boom Near term, I believe economic growth is likely to be challenged from the lagged effects of policy rates and tightening financial conditions. Long-term investors will be well advised to keep an eye on the horizon. Typically, building a supply chain takes 5-10 years, a process characterized by a front-loaded phase of intense commodity and labor demands followed by years of positive contributions to growth. In my view, we are in the early stages of a secular boom in commodities, with demands for energy, the energy transition, housing, infrastructure and electrification particularly likely to intensify.

These pressures are also likely to keep inflationary pressures at hand because labor markets remain tight, especially in construction and manufacturing jobs in the faster-growing South and Southwest. Nearshoring and onshoring are positive for long-term growth and employment, but they also reinforce that the baseline inflation rate is likely to be higher than in previous cycles.